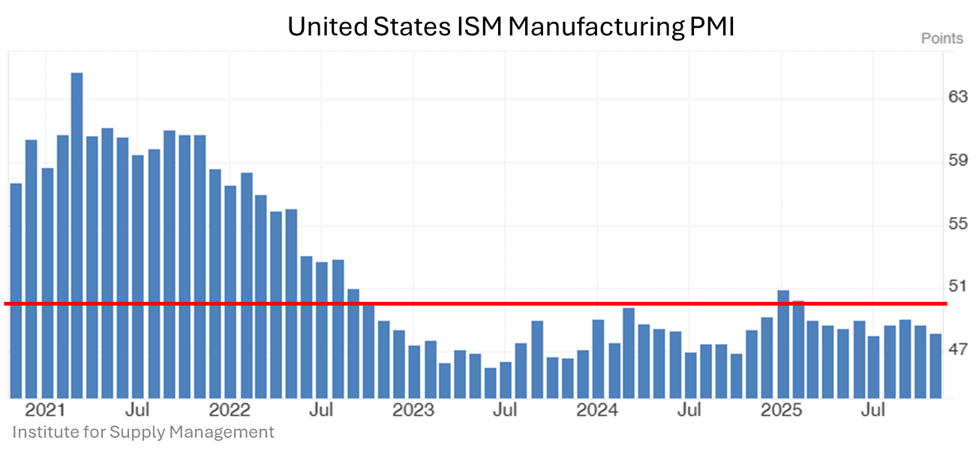

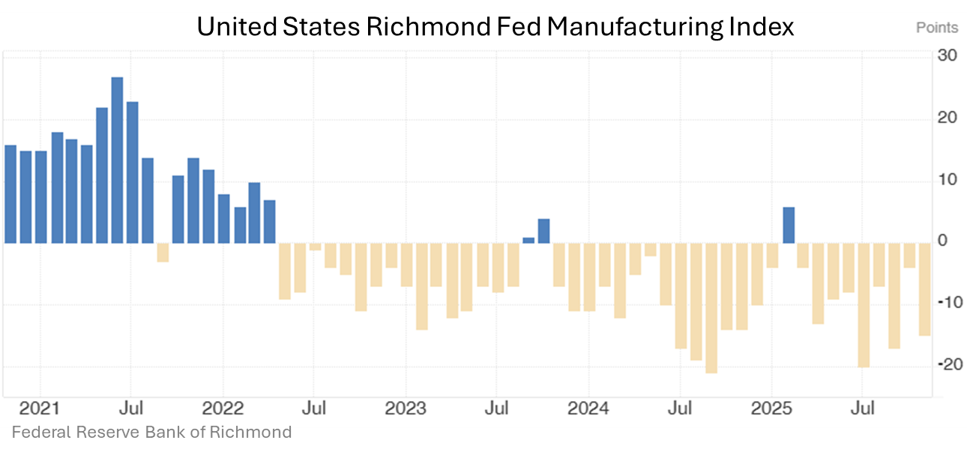

In 2022, both the U.S. Purchasing Managers’ Index (PMI) for Manufacturing and the Richmond Fed Manufacturing Index moved from expansion into contraction, and they have stayed there. For those of us focused on strengthening domestic manufacturing and rebuilding industrial capability, this shift is not just a data point. It signals real stress inside the production economy of the United States.

(The PMI shows whether U.S. manufacturing activity is expanding or contracting, where readings above 50 indicate growth in production and new orders, and readings below 50 indicate that the sector is shrinking.)

(The Richmond Fed index measures manufacturing conditions across the Fifth Federal Reserve District, where values above zero reflect improving activity and values below zero represent deterioration in output, orders, and employment.)

So what happened?

Why, after the post-pandemic rebound, did manufacturing stall instead of climbing back?

The answer is not one cause. Multiple pressures converged: supply problems, input cost inflation, weaker demand, and a pullback in capital investment. The downturn that followed was the result of these factors building on each other.

1. Supply chain disruption was the first domino to fall

The pandemic created shortages of semiconductors, metals, electronics, transportation capacity, and other critical inputs. These problems did not clear quickly. Instead, they became chronic.

Research from the Federal Reserve Bank of Cleveland found that problems in supply chains were the single largest contributor to cost increases between 2020 and 2022. When manufacturers cannot source the materials they need, production slows even when customer demand is healthy.

One delay in a global chain can stall entire sectors. Higher lead times, uncertainty, and planning difficulty all reduce output. Over time, those pressures pull manufacturing indexes downward.

2. Inflation squeezed margins and reduced the incentive to produce

Demand for goods returned quickly after lockdowns, but supply could not match it. The result was a surge in input costs. Both Federal Reserve research and industry analysis agree that costs for materials, freight, labor, and energy rose faster than many firms could pass along in pricing.

When a manufacturer sees orders increasing but profits shrinking, caution replaces growth. Output slows. Expansion plans pause. Confidence wavers.

Those decisions show up in PMI component scores for production volume, new orders, and capacity utilization.

3. Higher interest rates restricted investment in equipment and facilities

In 2022 the Federal Reserve raised interest rates sharply to control inflation. Capital intensive industries feel that more than most. When borrowing becomes expensive, companies think twice about:

- New equipment

- Plant expansion

- Advanced technology adoption

- Inventory financing

Several national industry surveys show a meaningful decline in manufacturing construction and equipment spending through 2022 and 2023. That pullback in investment aligns closely with the downturn in manufacturing activity. When businesses stop modernizing or expanding, overall output stagnates.

4. Demand softened, inventories increased, and production scaled back

By late 2022, order rates dipped. Consumers shifted spending toward services such as travel and hospitality instead of durable goods. Export demand cooled as other economies slowed.

At the same time, inventories that were built up during recovery became harder to move. When inventory rises and new orders fall, factories slow production to rebalance. Companies often freeze hiring or trim shifts. The result is a contraction cycle that reinforces itself.

5. The deeper challenge is structural

The decline was not only economic. It exposed weaknesses that have existed for decades within the U.S. manufacturing ecosystem. Among them:

- Global supply dependence with limited domestic redundancy

- Slow adoption of new manufacturing technologies

- Underinvestment in modernization and capital equipment

- Vulnerability to supply shocks and price volatility

When stress hit the system, it did not flex. It cracked.

These weaknesses help explain why recovery has not returned manufacturing to pre pandemic strength. Even as some supply disruptions eased, confidence and investment did not fully rebound. Costs remain high. Supply chains remain fragile. Managers are cautious.

What this means for manufacturers and for those helping them compete

The evidence is consistent. The downturn in manufacturing was driven by supply chain disruption, inflation in material and component costs, weaker order flow, and reduced capital spending. Each factor amplified the others.

If U.S. manufacturing is going to recover in a meaningful way, the path is not passive. It will require:

- Modernization with lower risk and better planning

- Tighter, more resilient supply networks inside the United States

- Clear business cases for technology adoption such as metal additive manufacturing

- Investment that is supported rather than deferred

This is where organizations like GENEDGE can help. Our work with Virginia manufacturers focuses on practical evaluation, disciplined planning, and technology adoption that improves competitiveness. If metal additive manufacturing is right for a company, we help build the roadmap. If it is not, we help determine that as well.

The contraction that began in 2022 showed the cracks in the industrial base. The opportunity ahead is to rebuild strength. That means a manufacturing sector that is more resilient, more advanced, and more capable of supporting the nation.

-Tony Cerilli, MEP Center Director

Feburary 2026 Update: New data reinforces continued pressure on U.S. manufacturing

Recent publicly reported economic data suggests that the headwinds described above have not meaningfully eased. Manufacturing activity remains uneven, hiring has softened in parts of the sector, and investment decisions continue to be shaped by cost pressures, policy uncertainty, and global competition.

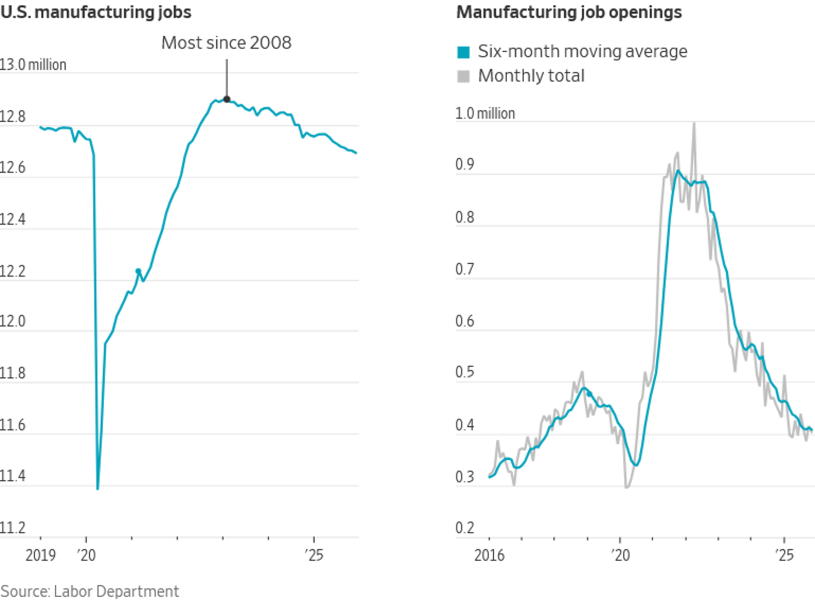

Federal employment data shows that manufacturing job growth has slowed and, in some periods, reversed across multiple subsectors since 2023. While layoffs have not spiked dramatically, hiring has been cautious and the overall trend points to a gradual pullback rather than expansion. This aligns with continued contraction readings in factory activity surveys and reinforces the view that the sector has been stabilizing at a lower level rather than rebounding.

Tariffs and trade policy remain a mixed factor. Over the long term, protective measures may support domestic production in certain industries by narrowing price gaps with imports. In the near term, however, many manufacturers continue to report higher input costs for materials and components that are still sourced globally. When key inputs are not readily available from U.S. suppliers, firms are often forced to absorb higher costs, raise prices, or delay investment decisions.

At the same time, the broader economic environment continues to play a major role. High borrowing costs over the past two years have limited capital expansion, and some downstream markets such as housing, automotive, and consumer durables have experienced periods of softer demand. Because manufacturing is tightly linked to these sectors, slowdowns ripple quickly through supply chains.

There are also signs of gradual stabilization in certain areas. Productivity improvements, process efficiencies, and selective domestic investment announcements suggest that output may be leveling off in parts of the sector, even if employment growth remains limited. In some cases, gains in efficiency mean that future production increases may not translate into large increases in headcount.

Taken together, the latest data reinforces the central theme discussed earlier in this post. The contraction that began in 2022 was not driven by a single event, and the path forward will not hinge on a single solution. Trade policy, interest rates, supply chain resilience, input costs, and long-term capital investment all continue to shape the trajectory of U.S. manufacturing.

What we are seeing now looks less like a sharp decline and more like a prolonged period of adjustment. The sector is searching for its footing in a new environment defined by higher costs, shifting supply networks, evolving technology, and uncertain demand signals.

-Tony Cerilli, MEP Center Director